Roughly 2.2 million Americans apply for Social Security Disability Insurance every year, according to the Social Security Administration — and nearly two out of three are denied on their first attempt. Most wait months just to receive that initial answer. What those numbers cannot capture is what the waiting actually costs a family in the meantime.

I first heard Janine Velasquez’s voice on a Tuesday afternoon in mid-March 2026. She was a caller on a Little Rock talk radio segment about rising healthcare costs and government benefits. She said, plainly and without much preamble, that her health insurance was costing her more than her rent. The host moved on after about ninety seconds. I wrote down her first name and called the station.

It took three days to track her down. When I finally sat down with Janine Velasquez at a diner on Cantrell Road in Little Rock, she arrived in her FedEx uniform, still on a modified shift, and ordered just coffee. She had the specific, exhausted composure of someone who has explained her situation too many times and still has not been heard.

When the Job That Paid Your Bills Starts Breaking Your Body

Janine has driven delivery routes for FedEx for six years. She is 33, married to Marcus, who works part-time stocking shelves at a grocery store for roughly $820 a month, and they have twin daughters — Lily and Mia — who turned seven in January. By any honest description, they are a working family without much cushion.

On October 14, 2025, Janine was unloading a pallet of heavy packages from her truck when she felt something give in her lower back. She kept working that day. She kept working for two more weeks after that, because stopping was not a financial option she felt she had. By early November, the pain was affecting her ability to drive a full route, and her doctor restricted her to part-time hours.

That reduction in hours triggered a cascade she had not anticipated. Full-time FedEx employees receive employer-subsidized health coverage. Drop below a certain hour threshold, and that coverage ends. Janine lost her employer health benefits on December 31, 2025. She received her COBRA election notice the first week of January 2026.

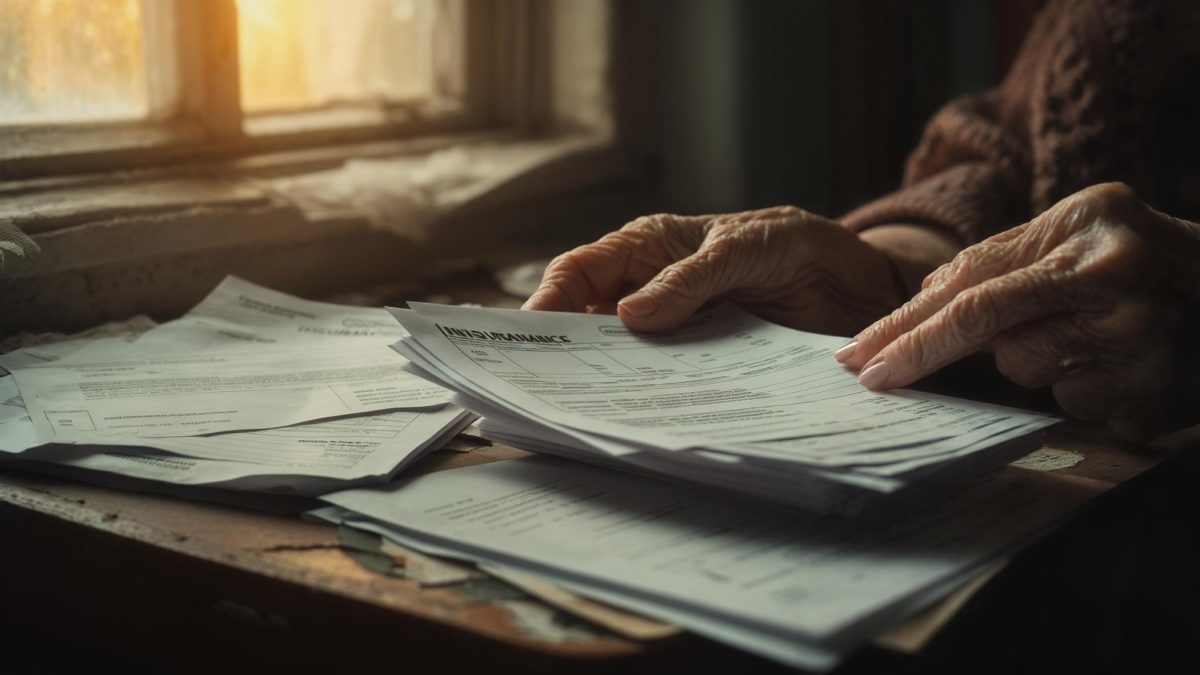

“Our COBRA is $1,847 a month,” Janine told me, her voice flat. “Our rent is $1,650. I didn’t even know that was legal until I got the paperwork.” Under federal law, COBRA allows workers who lose employer coverage to continue that coverage — but they must pay the full premium, including the portion their employer previously covered, plus a 2 percent administrative fee. For a family plan, that number can be staggering.

Janine’s take-home pay on part-time hours dropped to approximately $1,600 a month. Marcus brings in $820. Their total household income in January 2026 was roughly $2,420 — and their health insurance alone was consuming $1,847 of it.

The Roof, the Remittances, and the Running Out of Room

The COBRA bill was not the only financial pressure bearing down on the Velasquez household. In February 2026, a roofing contractor gave Janine an estimate of $8,400 to repair damage from a storm the previous fall. She did not have $8,400. She does not have $8,400 now.

Janine also sends approximately $300 a month to her mother in San Antonio, who is 61, widowed, and not yet eligible for Medicare or Social Security retirement benefits. “I can’t stop sending that money,” Janine said. “She doesn’t have anyone else. But I’m sitting here doing the math at midnight and the numbers just don’t work.”

When I told Janine that her income reduction might qualify her family for substantial subsidies on a Marketplace plan — potentially reducing their monthly premium well below $1,847 — she went quiet for a moment. She said no one at the COBRA administrator’s office had mentioned that. No one at FedEx HR had mentioned it either.

Filing for SSDI — and Learning What “Processing Time” Actually Means

On February 18, 2026, Janine filed an application for Social Security Disability Insurance. SSDI is a federal program that pays monthly benefits to workers who have a qualifying disability that prevents them from performing substantial gainful activity. To be eligible, applicants must have worked and paid Social Security taxes for a sufficient number of years — what the SSA calls “work credits.” Janine, with six years at FedEx, had enough credits to apply.

What Janine did not fully understand when she filed was how long the process would take. According to SSA guidance, initial decisions on SSDI applications typically take three to six months. If denied — which, statistically, most first-time applicants are — the appeals process can extend the timeline by another year or more.

“I’m working in pain every day,” Janine told me. “You’d think there’d be some kind of safety net for that. But I call the SSA number and I’m on hold for an hour and forty minutes.” She said she eventually hung up and submitted a question through the SSA’s online portal instead. She has not received a response.

Her frustration is not irrational. The SSA has faced ongoing staffing shortages and processing backlogs, a situation that has drawn scrutiny from advocates and policymakers alike. For a family spending down savings at the rate Janine’s is, six months is not an administrative inconvenience — it is a structural crisis.

Where Janine Stands Now — and What Remains Unresolved

When I spoke with Janine in late March 2026, she had been on COBRA for three months. Their savings — roughly $4,200 at the start of January — were down to approximately $800. The roof was still leaking. She was still driving, still in pain, still sending money to her mother in San Antonio.

She had not yet explored Marketplace coverage, partly out of fear. “What if I drop COBRA and something happens to one of the girls before a new plan kicks in?” she asked. “I don’t know enough about how the timing works to risk it.” That fear — of a coverage gap during a switch — is common and understandable, though insurance navigators and state assistance programs exist specifically to help families work through those transitions.

Her SSDI application status, as of our conversation, was simply “pending.” She had received one automated acknowledgment from the SSA. Nothing since. She checks the online portal every few days. “I filed in February,” she said. “It’s like I threw a letter into a hole in the ground.”

Janine Velasquez is not someone asking for sympathy. She was, in her own words, angry — at a system she pays into every paycheck, that she cannot fully access when she needs it, that communicates in forms she was never taught to read. The anger was quiet and specific, the kind that comes from having tried to do everything right.

What happens to her application — whether it is approved, denied, appealed, and eventually resolved — is still unwritten. I told her I would follow up when there is a decision. She shrugged and finished her coffee. “I’ll still be here,” she said. “Somewhere.”

Related: COBRA Cost This Jacksonville Mom More Than Her Rent. She Told Me She’s Just Going Through the Motions

Related: The SSA Said $0. An Advocate Said Otherwise — One Fresno Family’s 14-Month Fight for a Disabled Child’s SSI Benefit

Leave a Reply