If your income dropped by a third overnight and you had to choose between filling a prescription and paying a bill that was already weeks overdue, what would you reach for first?

I wasn’t expecting to find a story at a Walgreens on Fleur Drive in Des Moines on a Tuesday afternoon in February 2026. But when I heard a woman at the counter quietly asking the pharmacy tech about patient assistance programs — her voice steady, her hands gripping her purse strap tight — I waited. When she stepped away, I introduced myself and explained what I do.

That’s how I met Janine O’Brien, 59, a licensed plumber who has spent nearly three decades crawling under houses and threading pipe in commercial kitchens across central Iowa. She is the kind of person who fixes things for other people for a living and bristles visibly at the thought of asking anyone for help. She agreed to talk, though she took a long pause before she did.

From the Job Site to Disability — and Into Medicare at 59

In March 2023, Janine was on a commercial renovation job when she slipped on a wet concrete floor and tore two discs in her lower back. The surgery that followed kept her out of work for months. When it became clear she couldn’t return to full-duty plumbing work, she applied for Social Security Disability Insurance.

“I fought it,” she told me, sitting in her car in the pharmacy parking lot, the heat running against the February cold. “I didn’t want to be somebody who takes from the system. But I paid into it my whole life, and I genuinely could not work the way I used to.”

Her SSDI application was approved in October 2023, with a monthly benefit of $1,340 — a significant fall from the roughly $4,100 she had been bringing home each month, including overtime. Her husband, a warehouse supervisor, earns about $38,000 a year. Between them, they are raising four children from their respective first marriages.

What Janine hadn’t anticipated was that after 24 months on SSDI, she would automatically become eligible for Medicare — well before the standard age-65 threshold. That enrollment window opened in November 2025. She was 58 at the time, and suddenly faced a decision she had not prepared for: which Medicare coverage to choose.

The $0-Premium Plan That Seemed Like the Only Option

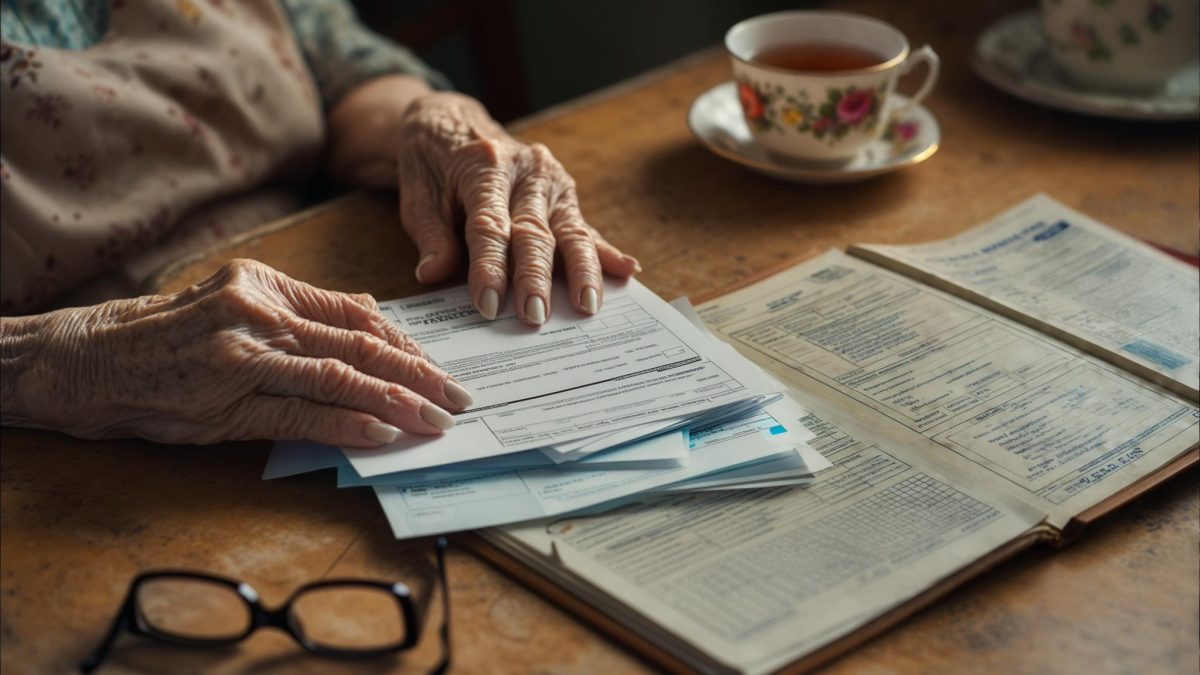

With property taxes behind by $1,840 and a garnishment notice on her kitchen table for an old credit card balance of $3,400, Janine was not in a position to absorb a meaningful monthly premium. When a mailer arrived advertising a Medicare Advantage plan with a $0 monthly premium and included dental and vision benefits, it looked like the obvious answer.

“I didn’t understand the difference between Medicare Advantage and regular Medicare,” she told me frankly. “I just saw zero dollars a month and thought, okay, that’s the one I can afford right now.”

She enrolled in the Medicare Advantage plan in November 2025. The premium was indeed $0. But what the mailer didn’t foreground — and what Janine didn’t know to ask — was how the plan’s prior authorization requirements and narrower provider network would play out in her specific situation.

When the Plan Said No

The first major friction came in January 2026, when Janine’s orthopedic doctor ordered a follow-up MRI to monitor her post-surgical spine. The Medicare Advantage plan required prior authorization before approving the scan. That request was denied — the plan determined the procedure wasn’t “medically necessary” under its criteria at her stage of recovery.

“I just sat there and cried,” Janine said, her voice dropping. “My doctor ordered this. It’s not like I’m asking for something optional. My back was operated on.”

She filed an appeal. The process took 19 days. The MRI was eventually approved, but by then her scheduled appointment slot had been filled. She waited another three weeks for a new one. In the meantime, she was managing pain with prescription medications that combined cost her $67 per month in co-pays — money pulled from the family grocery budget.

This experience is not rare. Discussions among Medicare enrollees — including in forums tracked by r/medicare on Reddit — consistently surface concerns about prior authorization denials and limited network access, particularly for enrollees managing chronic or complex conditions. The recurring finding is that these plans aren’t fraudulent, but they carry structural trade-offs that many people are never told about before they sign up.

The Bill She Didn’t See Coming

The larger blow arrived in February 2026. Janine had completed six physical therapy sessions recommended by her surgeon as part of her ongoing recovery. After the final session, she received an Explanation of Benefits showing that two of those six visits had been partially denied. The plan determined the billing codes submitted by the physical therapy practice didn’t align with its coverage criteria for post-surgical rehabilitation at her particular stage of treatment.

The balance she owed after the plan’s payment: $1,140.

“I had no idea those sessions might not be covered the same way,” Janine told me. “I showed my insurance card. Nobody at the PT office said anything. I got the bill a month later.”

She is now on a payment plan with the physical therapy practice — $95 per month — which she is managing alongside the garnishment payments and the property tax arrearage. As of early April 2026, none of the three debts has been cleared.

What Janine Knows Now — and Wishes She’d Known Before

When I asked what she would tell someone newly on Medicare, low income, trying to figure out which plan to choose, Janine didn’t pause to think.

“Ask what’s actually in your network before you sign anything. Ask how the prior authorization works. Don’t just look at the premium.”

She is now reviewing her options ahead of the next enrollment period. A social worker at her orthopedic clinic mentioned — in passing — that she might qualify for a Medicare Savings Program, which can help low-income beneficiaries cover premiums and cost-sharing. It was the first time anyone had brought it up. She hadn’t heard of it before that conversation.

By the time I started my car to leave that parking lot, Janine had already shifted back into the quiet, practical mode she seems to operate in by default. She thanked me for listening, then mentioned she needed to get home to start dinner. She didn’t want her kids to worry about things they couldn’t do anything about.

Her story is not one of catastrophic failure or dramatic rescue. It is something more ordinary, and in some ways more instructive: a capable, independent person who made a reasonable decision with incomplete information, and is now working through the consequences one payment at a time. That gap between what a plan appears to offer and what it actually delivers in practice is where a lot of people get hurt — quietly, without headlines, in pharmacy parking lots and at kitchen tables across the country.

Related: She Didn’t Know Her Ex Was Hiding Income. Then the IRS Sent Her a $8,400 Bill.

Related: My Father’s Social Security COLA Bump Was $35 a Month. His Medicare Premium Ate $27 of It.

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply