What would you do if your household income crossed $76,000 a year, but you still couldn’t pay your property taxes, fix your roof, or keep up with an upside-down car loan — all because your child’s survival depended on a government program that might not survive the next budget cycle?

I found Randall Trujillo the way I find a lot of people worth writing about: in the comments section. He left a long, unfiltered post under my piece on Medicaid waiver programs for children with disabilities, and it stopped me mid-scroll. Three days after I reached out, I was sitting across from him at a diner on Chicago’s Northwest Side, watching him wrap both hands around a coffee mug like it was the only solid thing in the room.

Randall is 57, a licensed pest control technician who has worked for the same commercial extermination company for nine years. He and his wife, Denise, bring home approximately $6,400 a month. By most definitions, that is solid, working-class stability. By Randall’s definition, it is not close to enough.

A Budget That Doesn’t Add Up No Matter How Many Times You Run It

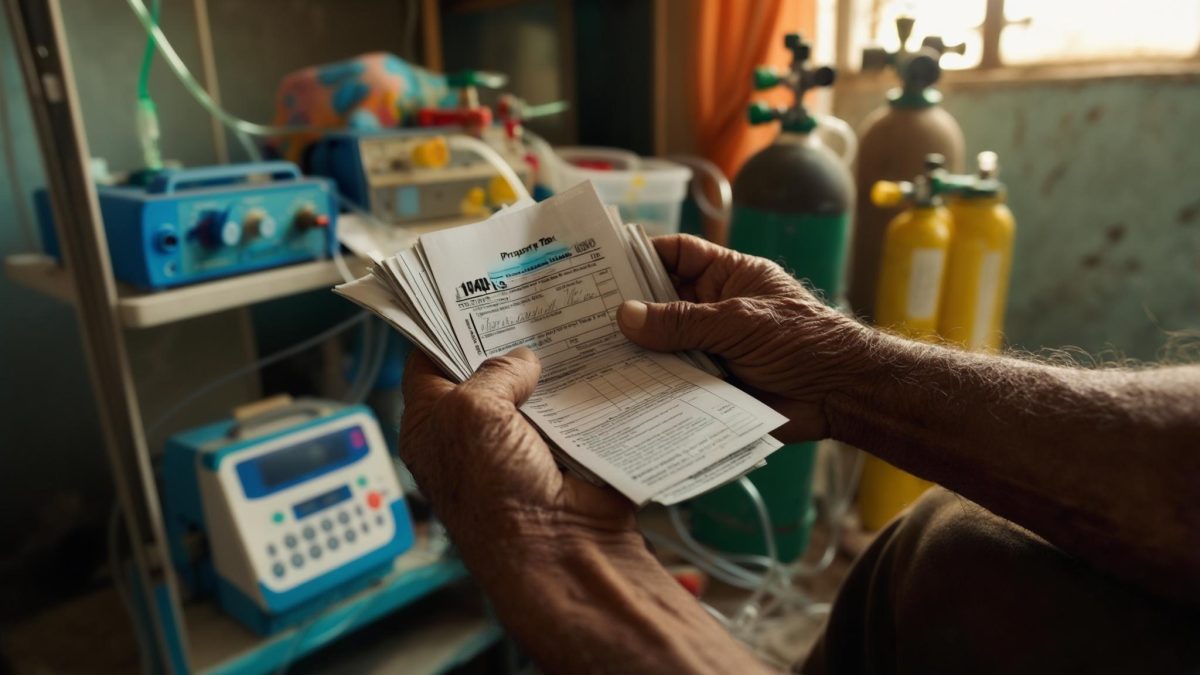

The numbers Randall laid out for me were striking in their specificity. He and Denise are $4,800 behind on Cook County property taxes — a balance that has been accruing penalties since October 2024. Their 2019 Ford F-150 is worth roughly $18,000 on today’s market, but they owe $24,600 on it, leaving them $6,600 underwater. The house they bought in 2017 needs a new roof and HVAC system, a combined repair estimate of $21,500 that has sat on the kitchen counter, largely unread, since February.

None of this reflects carelessness. It reflects the true cost of raising a child with severe autism in a system not designed for families like theirs. Randall and Denise’s 15-year-old son, Mateo, requires full-time behavioral and therapeutic care. Before Mateo was enrolled in Illinois’s Medicaid Home and Community-Based Services waiver program in 2022, the family was paying $3,200 a month out of pocket for a combination of Applied Behavior Analysis therapy and a part-time behavioral aide.

That $3,200 monthly spend consumed everything that might have gone toward savings, debt payoff, or maintenance. Randall described the years between 2018 and 2022 as a slow-motion financial collapse in which every choice was between Mateo’s therapy and something else the family needed just as badly.

“I make decent money. I always have,” he told me. “But decent money doesn’t mean anything when you’ve got a kid whose needs cost more than a second mortgage every single month.”

The Waiver That Saved the Family — and the Threat Following Close Behind It

Illinois’s Medicaid HCBS waiver operates on what’s sometimes called a Katie Beckett model: it allows children with significant disabilities to access Medicaid benefits regardless of parental income. As HHS explains, Medicaid covers services that Medicare doesn’t normally provide — including personal care, long-term support, and home-based services. That is precisely what Mateo needs, and what no private insurance plan has ever agreed to cover at a meaningful level.

Once enrolled, Mateo’s behavioral health services, respite care, and therapeutic supports have been covered at essentially no cost to the family. The waiver did not just save Randall money. It saved his marriage, he told me, with no exaggeration in his voice.

That relief is now shadowed by a new and very specific anxiety. In 2026, state Medicaid programs are under fiscal pressure that advocates describe as unlike anything in recent memory. The implementation of the 2025 reconciliation law is squeezing state budgets, and Medicaid — particularly waiver funding for disability services — is directly in the crosshairs. According to Fortune’s analysis of federal benefit solvency, recent federal tax cuts have shortened the projected stability window for programs including Medicaid.

Randall has been following budget headlines the way other people follow sports scores — obsessively, with a sense that the outcome personally determines his family’s future. He reads every CBO update, every state legislative summary. He said he feels perpetually angry but struggles to identify a single target for that anger.

“The politicians all say they’re protecting these programs,” he told me, leaning forward. “Then you read the actual numbers and you think — wait, who’s lying to me? Because someone is. It feels like everyone is.”

What the 2026 Social Security and Medicare Changes Mean for Someone in Randall’s Position

Randall is 57. Social Security is a decade away, but he has started doing the math because he has no choice — retirement planning when you’ve spent years financially treading water requires an early start just to get to even.

The 2026 Social Security changes are not abstract to him, even if they don’t affect him yet. According to AARP’s breakdown of 2026 Social Security changes, current beneficiaries are receiving a 2.8% cost-of-living adjustment this year. That sounds like meaningful relief — until you factor in that the Medicare Part B premium is simultaneously rising from $185 to $202.90 per month. Research from the Center for Retirement Research at Boston College found that higher Medicare premiums will consume more than 25% of that COLA for many retirees before it ever appears in their bank accounts.

Randall is a decade from Medicare eligibility, but the dynamic matters to him because his employer-sponsored health insurance currently costs the family $680 a month in premiums alone — and it does not touch the specialized care Mateo receives through Medicaid. If Mateo’s waiver is cut or restructured, no private plan he can afford provides a real backstop.

He told me he has run the scenario of early Social Security filing at 62 versus waiting until his full retirement age of 67. Every time, the numbers point to waiting. Every time, he wonders whether waiting is a luxury he’ll actually have.

Where the Trujillo Family Stands in April 2026

When I asked Randall what he wanted readers to take away, he paused for a while. He is not someone who wraps things up cleanly.

The property tax bill is still outstanding. Randall and Denise are working with Cook County’s installment payment program to avoid a tax sale, but penalties accumulate each month. The truck they’re locked into until the balance aligns with the vehicle’s value. The roof estimate remains on the counter.

What has shifted is Randall’s understanding of how fragile all of it is. He assumed that once the waiver was approved, the hard part was over. He knows now it was only the beginning of a different kind of work — advocacy, documentation, monitoring, showing up to meetings, writing letters, reading bills.

I left that diner thinking about the particular cruelty of Randall’s situation — not because he is uniquely unlucky, but because he represents a category of American family that no program is cleanly designed to serve. He earns too much to qualify for most assistance himself, but not nearly enough to absorb the actual cost of a child with complex needs. He works hard, files his taxes, shows up every day to a job that requires him to crawl into dark spaces and solve other people’s problems.

He doesn’t know where to direct his anger. Sitting across from him, I wasn’t sure I could offer him anything that would help with that — and that felt like its own kind of answer.

(function(){var w=document.getElementById(‘pvv-scenario-s1775659842218c075’);if(!w)return;var btns=w.querySelectorAll(‘button[data-choice]’);btns.forEach(function(b){b.addEventListener(‘click’,function(){if(w.dataset.revealed)return;w.dataset.revealed=’1′;btns.forEach(function(x){x.style.opacity=x===b?’1′:’0.45′;x.style.cursor=’default’;x.style.transform=’none’});var o=document.getElementById(‘s1775659842218c075-out-‘+b.dataset.choice);if(o){o.style.display=’block’}});b.addEventListener(‘mouseenter’,function(){if(!w.dataset.revealed){b.style.borderColor=’#38bdf8′;b.style.transform=’translateX(4px)’}});b.addEventListener(‘mouseleave’,function(){if(!w.dataset.revealed){b.style.borderColor=’#334155′;b.style.transform=’none’}})})})();

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply