Most financial planning advice assumes that people who understand money are somehow protected from money anxiety. That assumption is wrong, and Carmen Norwood is living proof of it.

I met Carmen at a block party in south Minneapolis last September, introduced by a mutual neighbor who mentioned, almost in passing, that Carmen had recently started losing sleep over her retirement timeline. Carmen didn’t volunteer much that evening — she’s not the type — but she agreed, a few weeks later, to sit down with me at her kitchen table and walk through what was actually worrying her.

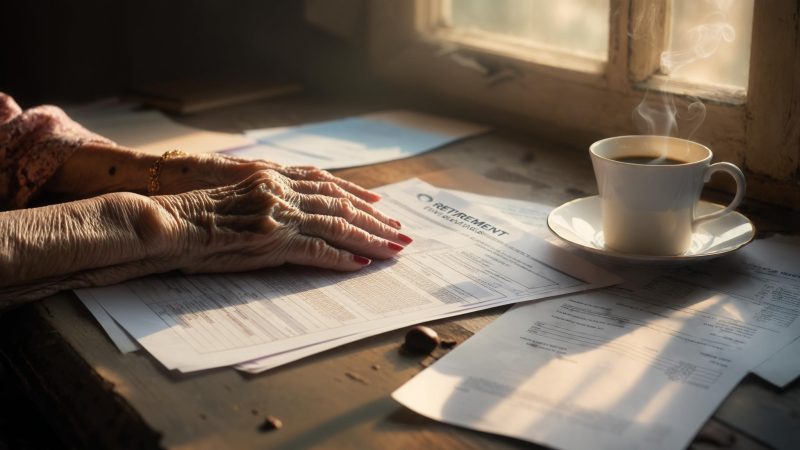

What I found was a 63-year-old senior accountant with more spreadsheet discipline than almost anyone I’ve interviewed, quietly panicking in a way she hadn’t told her husband, her daughter, or anyone in her family. “I keep the books for other people,” she told me early in our conversation. “It feels embarrassing to admit my own books don’t balance right now.”

A Budget Built on Overtime That Disappeared

Carmen has worked in accounting for 34 years. She and her husband, Marcus, a facilities manager, live in a modest home in the Powderhorn neighborhood. Their daughter, Destiny, is 17 and heading to college in fall 2027 — a milestone Carmen has been planning for financially since Destiny was in elementary school.

Until late 2024, Carmen’s household budget worked, but only barely. She had been pulling roughly $800 to $1,100 per month in overtime — a number she’d come to depend on to cover the gap between their base income and their monthly expenses, which run approximately $5,400. Then her firm restructured in November 2024, reclassified her role, and the overtime dried up almost completely.

“I went from putting away about $850 a month into my 403(b) to putting away maybe $200,” she told me. “That’s not a tweak. That’s a collapse.” She said it quietly, without drama, the way an accountant delivers bad news in a board meeting.

Her current retirement savings sit at approximately $187,000 — a number she described as “not terrible for someone my age statistically, but terrible for what I actually need.” With Destiny’s college costs looming (Carmen estimates $14,000 to $18,000 in parental contributions over four years), the margin for error has essentially disappeared.

Where Social Security Enters the Picture

Carmen’s plan, as she had sketched it out, assumed she would claim Social Security at 67 — her full retirement age — and receive approximately $2,140 per month based on her earnings record. She had checked her Social Security online account in January 2026 and confirmed the estimate. Marcus would claim at 65, bringing in an estimated $1,680 per month. Together, that’s roughly $3,820 monthly in Social Security income — the foundation of their retirement plan.

The problem is that foundation keeps moving.

Early forecasts for the 2027 COLA are calling for a 2.8% increase, matching 2026’s adjustment. According to 247 Wall St., rising oil prices could push that figure higher — but that’s not necessarily good news. A higher COLA driven by energy inflation means beneficiaries are already paying more for gas and utilities before the adjustment even arrives.

Carmen had read about this. She pulled up the numbers on her laptop while we talked, cross-referencing forecasts against her own projected benefit. “A 2.8% COLA on my estimated check is about $60 a month,” she said. “If Medicare Part B premiums go up at the same time — which they always seem to — that $60 gets eaten before I ever see it.”

The Trust Fund Number That Keeps Coming Up

I asked Carmen when she first started feeling genuinely anxious — not just careful, but anxious — about retirement. She thought for a moment and said it was a Sunday afternoon in October 2025, when she read a projection that Social Security’s trust fund could be depleted by 2032.

That’s not an outlier estimate. According to trust fund projections widely reported in early 2026, depletion around 2032 would trigger automatic benefit cuts — potentially costing a typical two-earner couple roughly $18,400 per year in lost income.

Carmen is not a catastrophist. She was careful to say she doesn’t believe benefits would disappear entirely — Congress has historically intervened before full depletion. But a partial cut, even of 20%, would reduce her projected household Social Security income from $3,820 to roughly $3,056 per month. That’s a $764 monthly gap that her depleted savings would need to cover, indefinitely.

She opened a spreadsheet she had built over several evenings in November 2025 and showed me the math. It assumed 3% annual inflation, 6% portfolio growth, and two people living to age 88. The savings runway, even under optimistic assumptions, ran out around age 81 — seven years short.

What Carmen Is Actually Doing About It

Carmen has not asked her siblings for help. She hasn’t told her parents, who are in their late 80s and live nearby. Her daughter doesn’t know the full picture. “Destiny thinks we’re fine,” Carmen said, with a short, tired laugh. “I want her to go to college without carrying this.”

What she has done is concrete and methodical, in the way you’d expect from someone who has spent three decades managing other people’s financial records.

The claiming age decision is one Carmen described as agonizing. Every year she delays past 62 adds roughly 5% to 8% to her permanent monthly benefit. But waiting also means burning through more savings during those early retirement years, assuming she retires at 65 or 66 as she hopes. “The math says wait,” she told me. “But the math also assumed I’d have more savings by now.”

The Regret She Didn’t Expect to Feel

Near the end of our conversation, Carmen said something that stayed with me. She said the hardest part isn’t the math — it’s that she did everything right for so long and still ended up here.

She maxed out her retirement contributions in her 40s. She paid off her car early. She didn’t take equity out of her house. She built an emergency fund. And then — a restructuring she couldn’t control, a daughter she wouldn’t sacrifice for the sake of a spreadsheet, a COLA that looks decent on paper but gets quietly eroded by Medicare before it ever hits a bank account.

She’s not in crisis — she was clear about that, and I believed her. Her home is paid off except for six years remaining on the mortgage. She has no credit card debt. She and Marcus are healthy. But she’s 63, and the window to course-correct is narrowing in a way it wasn’t five years ago.

The 2027 COLA forecast — currently estimated at 2.8%, though analysts at 247 Wall St. warn it could rise due to energy prices — represents both a small relief and a reminder of the system’s limits. A larger COLA sounds like good news until you realize it means inflation is accelerating faster than expected. For Carmen, who will be 64 when 2027 adjustments take effect, none of these numbers move fast enough to close the gap her overtime income left behind.

When I left her kitchen that afternoon, she was already back at her laptop. The spreadsheet was open. She was adjusting a variable — I didn’t ask which one — and frowning at the result. It looked exactly like someone running the numbers one more time, hoping they’ll come out differently.

They didn’t. But she kept running them anyway. That, more than anything, felt like the truest thing about Carmen Norwood.

Leave a Reply