Most people assume that earning a decent living means you’re on your own when a health insurance crisis hits. That assumption, it turns out, can cost a family tens of thousands of dollars — and nearly cost Darlene Peralta her financial footing entirely.

I first connected with Darlene in late February 2026, after a social worker at the Hennepin County Human Services office in Minneapolis suggested I speak with her. The social worker — who asked not to be named — described Darlene’s case as “one of the clearest examples I’ve seen of a working family falling into a gap nobody warns them about.” When I reached Darlene by phone the following week and then met her in person at a coffee shop near her home in the Longfellow neighborhood, she agreed immediately to share her story.

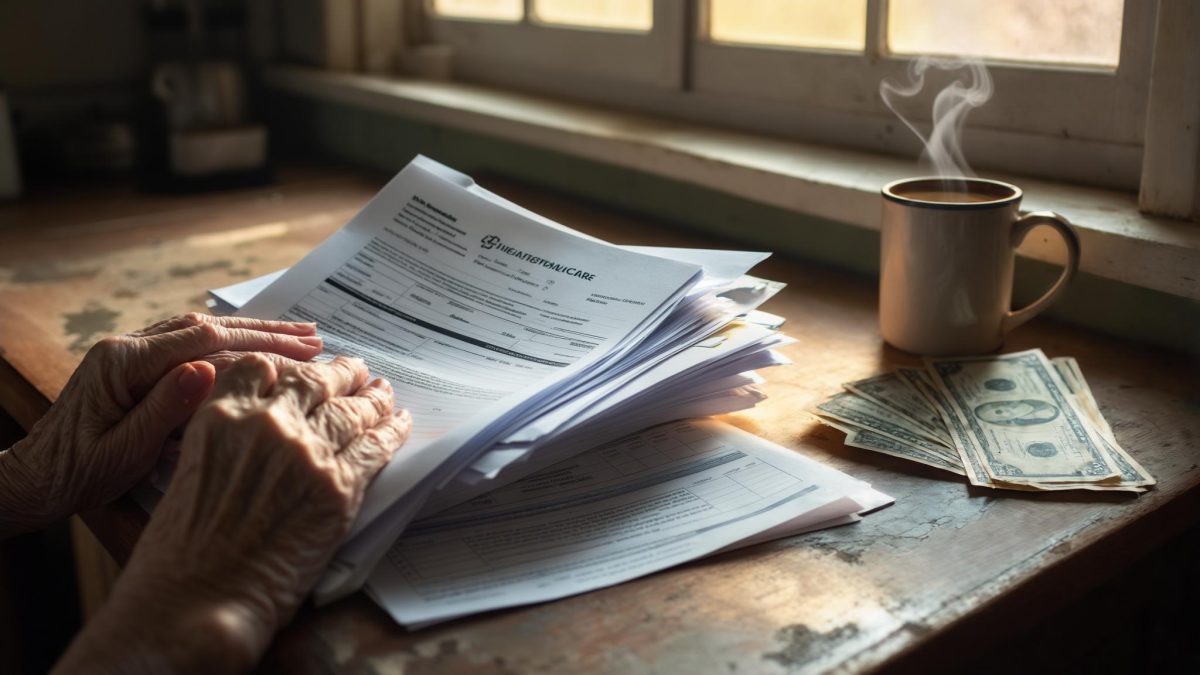

“I want other people in my situation to hear this,” she told me, wrapping both hands around a coffee mug. “Because I sat with this for eight months before anyone told me I had options.”

A Blended Family, a Job Transition, and a Bill Nobody Was Prepared For

Darlene Peralta is 33 years old, works as an insurance claims adjuster, and lives in Minneapolis with her husband Marcus and their four children — two from her previous relationship, two from his. On paper, the household looks stable. Marcus earns roughly $74,000 a year as a project coordinator; Darlene brings in approximately $68,000. Together, they clear well over $130,000 annually.

But the picture changes quickly when you start layering in the actual expenses. Marcus’s ex-partner has not paid court-ordered child support in over a year — a balance that had climbed to approximately $9,200 in arrears by January 2026, according to Darlene. The couple is also behind on property taxes, owing roughly $5,100 to Hennepin County after a missed payment in the fall of 2024 cascaded into penalties.

The breaking point came in June 2025, when Darlene left her previous employer to take her current position. There was a 47-day gap between when her old coverage ended and when her new employer’s plan kicked in. She elected COBRA to bridge that window — and received her first bill shortly after.

“I knew it was going to be expensive,” she said. “I did not know it was going to be $2,340 a month.”

When the Health Insurance Bill Exceeds the Mortgage

To put that number in context: Darlene and Marcus pay $2,190 per month on their mortgage. Their COBRA premium, which covered all six family members, was $150 more than their housing payment — every single month.

For 47 days, that was mathematically unavoidable. What Darlene did not realize — and what nobody at her former HR department mentioned — was that her children might have qualified for MinnesotaCare or the Children’s Health Insurance Program (CHIP) during that gap period, potentially reducing her out-of-pocket obligation substantially. According to Healthcare.gov’s CHIP overview, children in families earning up to 275% of the federal poverty level may qualify in Minnesota — a threshold that, depending on household size and calculation methodology, can reach into six-figure income ranges for larger families.

“No one at my old job said anything about that,” Darlene told me, shaking her head. “They handed me a COBRA election form and a deadline. That was the whole conversation.”

The Eight Months Nobody Said Anything

Darlene’s new employer plan kicked in on August 1, 2025. The COBRA crisis was technically over. But the financial damage had already compounded — and a new, quieter problem had taken root.

Her new employer’s family health plan carried a premium of $890 per month, which felt like relief after COBRA. But the plan came with a $6,000 family deductible and limited network access in the Twin Cities metro. When one of her younger children needed a specialist visit in September, the out-of-pocket costs added another $740 to the pile.

Meanwhile, the unpaid property taxes were accruing an 8% annual penalty under Hennepin County’s delinquency schedule, and the child support enforcement process — while ongoing — had produced no actual payments. By November 2025, Darlene said she and Marcus had drawn down nearly $11,000 from their emergency fund.

“We were managing,” she said. “But ‘managing’ meant we weren’t saving anything. We weren’t building anything. We were just keeping the lights on.”

The couple did not seek outside help during those months. Darlene said she assumed their household income made them ineligible for any assistance programs. “We make good money. I know that. I didn’t think we were the people who were supposed to call those offices.”

What Changed — and How a Social Worker Reframed Everything

In January 2026, Darlene went to the Hennepin County Human Services office — not for herself, she emphasized, but to help a neighbor navigate a Medicaid question. While she was there, a social worker named Patricia overheard a side comment Darlene made about their COBRA experience the previous summer.

What followed was a 40-minute conversation that Darlene described as “the most useful 40 minutes I’ve had in two years.”

“She wasn’t telling me anything exotic,” Darlene said. “These are programs that exist. They’re funded. They’re running right now. I just didn’t know to ask.”

According to CMS’s COBRA guidance, most employers are required to notify employees of their continuation coverage rights within 14 days of a qualifying event — but that notice does not include information about alternative coverage options like CHIP or state marketplace plans. The gap in disclosure is legal and common.

A Small Win — and the Fear It Won’t Hold

By March 2026, Darlene had enrolled her two youngest children in MinnesotaCare, reducing the family’s monthly health coverage costs by approximately $310. The Hennepin County property tax office had approved a 12-month repayment plan on the $5,100 balance — structured at $425 per month with no additional penalty accrual going forward. And the child support enforcement office had flagged Marcus’s ex-partner for a state tax intercept on their 2025 return.

These are not dramatic rescues. Darlene was careful to say that. The child support arrears have not been collected yet — enforcement actions can take months to produce actual payments, and there is no guarantee. The emergency fund has not been replenished. The family is still stretched.

She said the hardest part of the last year was not the financial pressure itself — it was the feeling that she should have known better. “I work in insurance. My husband manages project budgets. We’re not naive people. But this system is not designed to tell you what you qualify for. You have to already know to go looking.”

What Darlene’s Story Actually Reveals

Darlene Peralta is not a cautionary tale about reckless spending or poor planning. She and Marcus earn well above the median household income in Minnesota, which according to U.S. Census Bureau data sits at approximately $87,000. They own a home. They had savings. They did most things right.

What they encountered was a system that presents COBRA as the default — the only option — when in reality it is one option among several, and often the most expensive one. The absence of proactive disclosure about alternatives is not a glitch. It is simply how the system operates.

When I left the coffee shop that afternoon, Darlene walked me to the door and paused. “Tell people to go to those offices,” she said. “Even if you think you make too much. Even if you feel like you’re not the person those offices are for. Go anyway and ask.” She smiled, but it was the kind of smile that carries a lot of weight behind it — the smile of someone who got a small win and is quietly terrified of what comes next.

That, more than any number in this story, is what stayed with me.

Related: She Was Already Paying More for COBRA Than Rent. Then a Scammer Posing as Social Security Called.

Related: He Pays More for COBRA Than Rent Every Month. At 63, Harvey Underwood Has 731 Days Until Medicare

Leave a Reply